Fitness Industry Overview

U.S. Fitness Industry Outlook: Growth, Challenges, and Opportunities

2/9/20257 min read

Size and Overview

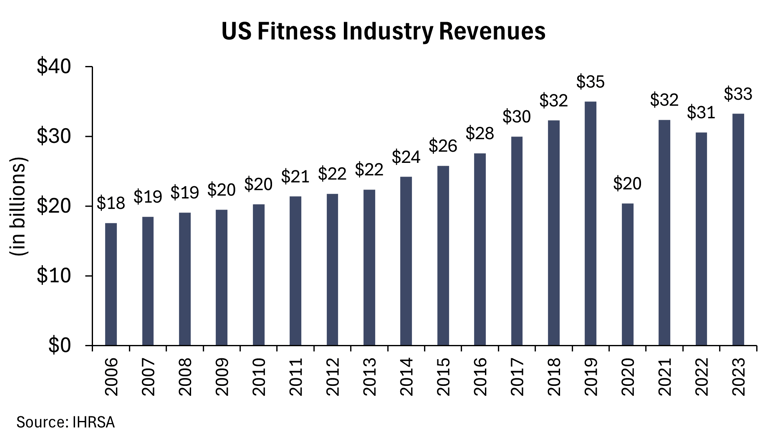

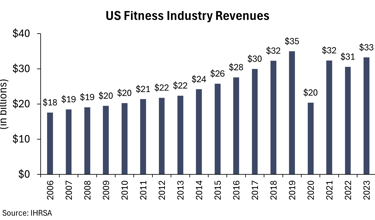

The US health & fitness industry, at a size of ~$33 billion, has nearly recovered from the pandemic and is expected to increase on a go-forward basis consistent with its historical CAGR of over 3%. Outside of the pandemic, the fitness industry has performed well during recessions with consumers typically maintaining their membership due to its relatively low-price point and health benefits. We expect the industry to remain defensive and stable during future economic slowdowns as evidenced by the stability exhibited during the Great Recession of 2008-2009.

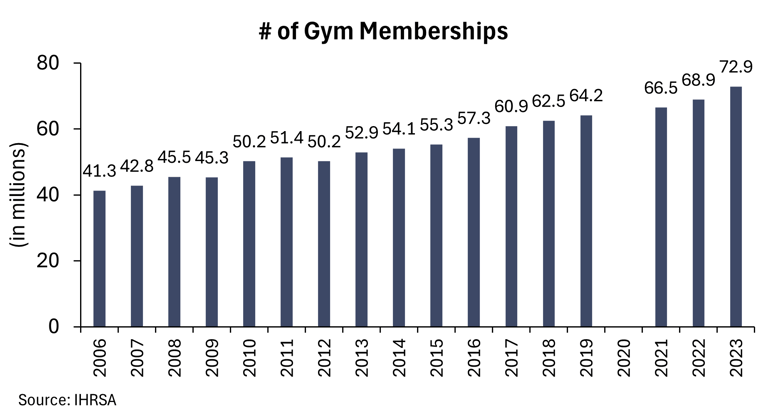

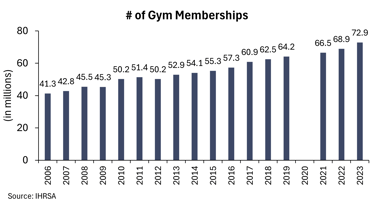

In tandem with industry revenues, the number of gym members has increased from ~50 million in 2010 to nearly 73 million in 2023 due to growing awareness for health and wellness and improved marketing from the likes of Planet Fitness, creating a larger total addressable market for industry participants.

Market Share

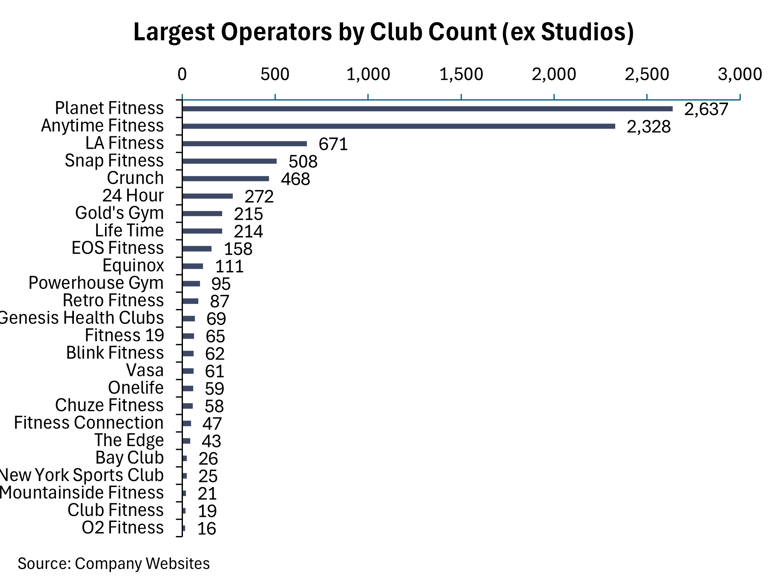

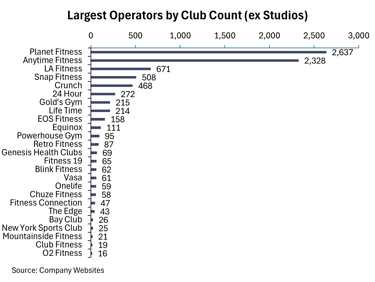

The fitness industry remains highly fragmented, consisting of a mix of independent gyms, boutique studios, regional operators, and national chains. According to industry data, the top 10 operators account for less than 30% of the market share, leaving meaningful room for growth and consolidation.

Industry Threats

Despite numerous threats over the years (P90x, wearable fitness technology, ClassPass, specialized studios, etc.), nothing has been able to replicate the in-person gym experience. In fact, studies have shown that gym memberships are positively correlated with at-home workouts as consumers continue to prioritize their membership with the digital flywheel unlocking even more value for members and supports retention. We expect gyms to remain relevant and for these trends to continue as Gen Z has a higher penetration of gym memberships compared to previous generations at the same stage. Also, surviving incumbents and emerging operators have adapted to stay relevant with the consumer through expanding their class offerings, providing at-home workout alternatives, and making the in-person experience social and fun.

Industry Categories

The fitness industry is broken out into four categories (High-End, Mid-Tier, Low Price, and Studios). Our thesis is a barbell strategy – invest in low-price and high-end clubs and avoid mid-tier operators and studios. Overall, our view is that the fitness category will continue growing due to structural drivers such as increasing gym membership penetration, as highlighted by Gen Z and the resilience that gyms have had over the decades despite several threats, most recently the pandemic. Moreover, health & wellness has become mainstream in our society with more widespread adoption in being active.

COVID Impact

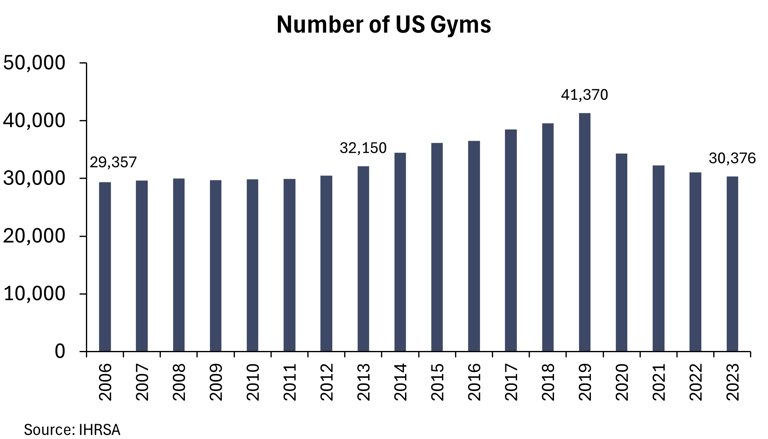

During the pandemic, gyms were forced to temporarily close, some for several months depending on the state. The uncertainty of this environment and the fixed cost component of gyms resulted in several bankruptcies (e.g., 24-Hour, Gold’s Gym, Town Sports). During this time period, there was the looming threat of at-home workouts led by the popularity of Peloton. However, gyms remained resilient and have nearly fully recovered revenues with industry players more profitable than pre-COVID as ~27% of gyms (primarily mom & pop) have permanently closed since the pandemic.

Industry Transformation

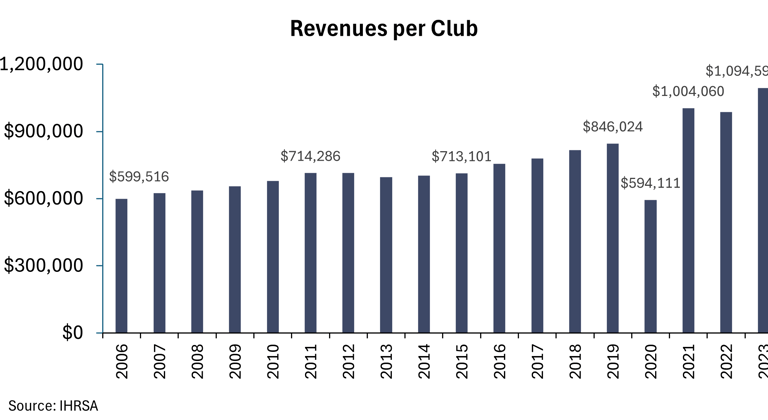

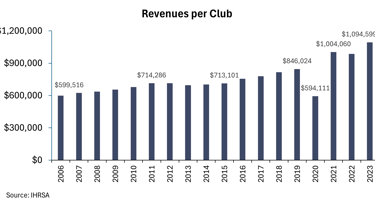

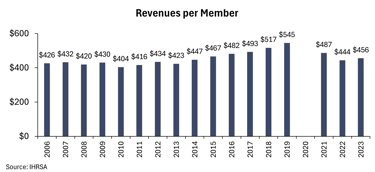

Despite ~27% fewer gyms, industry revenues are nearly back to pre-COVID levels and revenues per club are ~30% above pre-COVID levels as incumbents increased market share and exhibited strong pricing power through raising membership fees.

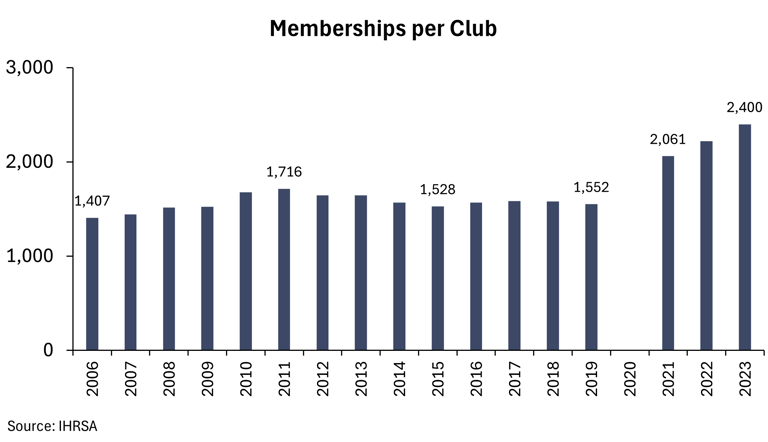

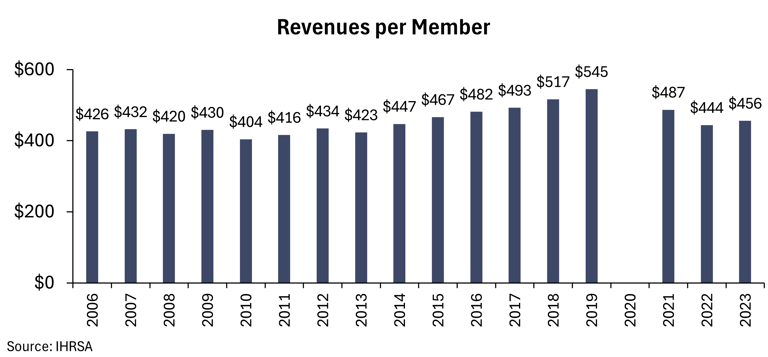

There has been a shift in the industry over the past decade towards the low-price category which has increased in popularity and has positively contributed to improving industry revenues per club with higher membership levels per club more than offsetting lower prices.

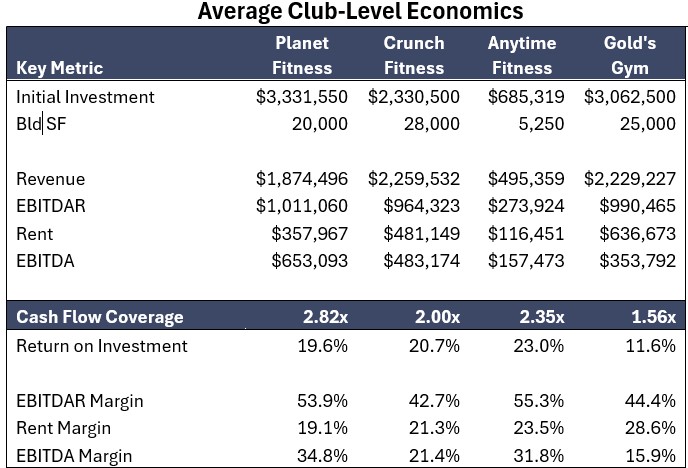

Due to strong unit-level economics and return on investment, the industry is expanding rapidly with new club growth. We expect these trends to continue, followed by increased consolidation once returns for opening new clubs decrease and new players take share from incumbents (similar to LA Fitness acquiring XSport).

Sources: FDDs

Low-Price Category

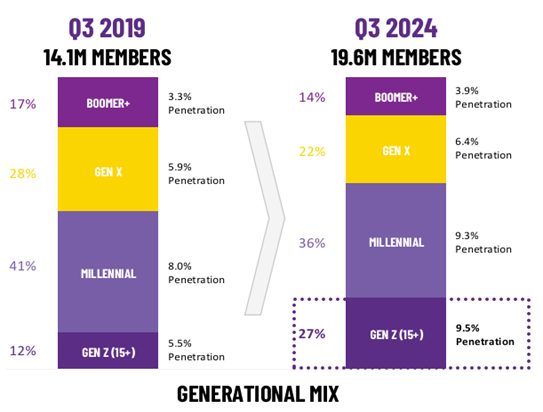

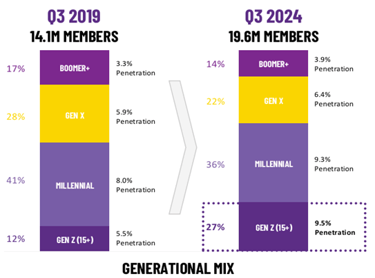

Planet Fitness is the leader in the low-price category, the fastest growing segment in the industry. Planet’s success has significantly increased the total addressable market, increasing gym members by 11.1 million from 2011 to 2019, accounting for ~85% of industry growth (12.8 million new gym members during the same time period).

Planet has done a fantastic job marketing to younger generations which has shown up in their membership counts. For example, Planet Fitness has a higher penetration of younger generations (9.5% currently vs. 5.5% in 2019) which is a positive sign for the entire industry as their marketing efforts have worked and they are enjoying the benefits of structural tailwinds (e.g., growing health and wellness awareness, social experience, etc.).

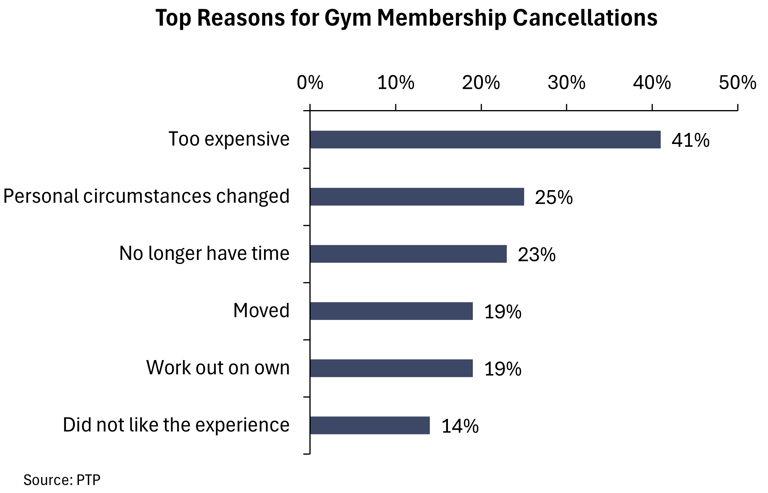

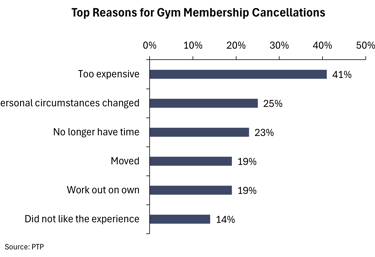

Due to Planet’s success, there has been a new wave of low-price operators that have disrupted the industry (e.g., VASA Fitness, EOS, etc.). This new class of gyms offer all the same amenities (e.g., kid’s club, pool, bb court, classes, etc.) as mid-tier operators but for roughly half the monthly membership price. The model has proven to be profitable by keeping operating costs low, attracting new members by providing a positive and uplifting atmosphere (e.g. ‘The Judgment Free Zone’ by Planet), and retaining more members by alleviating the main reason why gym-goers cancel their membership --- price.

While pricing power somewhat lacks in the low-price segment, operators have become more creative with increasing membership dues. Most gyms have 2-3 different membership levels and often the strategy is to gradually increase the higher-tier pricing and annual dues while keeping the headline rate low with no price increase for marketing purposes. However, Planet Fitness increased its headline membership price of $10 to $15 over the summer, marking its first increase in 25 years. The price increase had a minimal impact on membership attrition, highlighting that strong brands, even in the low-price category, have some pricing power. Additionally, over half of Planet’s members choose the higher membership tier as operators incentivize this behavior through improved membership benefits and a lower or no initiation fee.

Mid-Tier Gyms

The mid-tier segment is shrinking as incumbents face pricing pressure from alternative, low-price operators, and typically cannot replicate studio offerings or the high-end experience to command greater pricing power. The leader in the mid-tier category, LA Fitness rolled out Esporta in 2019 to better compete with low-price operators that were taking market share from them. The Company converted about 200 of its existing clubs to Esporta which was a failed experiment as the Esporta brand was unable to resonate with the customer. Aside from 13 remaining Esporta locations, all other clubs have been rebranded back to LA Fitness or closed.

High-End Clubs

The high-end space, led by Life Time, has been relatively stable. Memberships in this category have fallen since the pandemic but pricing has increased tremendously (~+40% for Life Time), resulting in more profitable centers and a more differentiated, country club experience for members. The high-end category has exhibited more pricing power than other fitness categories given its differentiated model and higher barriers to entry. While LA Fitness failed going downstream with Esporta, they have recently launched the ‘Club Studio’ concept to compete on the high-end space. The concept only has a few locations currently and is too early to gauge its success.

Studios

The final category, Studios, is a relatively new category, emerging on the scene in the early 2000s and gaining widespread popularity throughout the 2010s. Fitness studios are here to stay but individual concepts are difficult to invest in because fitness trends come and go with many concepts proving to be fads. Additionally, many of these studios fail to sustain profits given the challenges in hiring great instructors, revenue limitations from the limited number of classes offered per day, and increasing competition from gyms offering similar classes as part of their monthly package. Pre-pandemic, studios were the fastest growing category but gyms have invested in this space with their own in-house offerings to better compete. Nowadays, Studios are viewed less as a gym alternative but more as a gym supplement with their success driven by specialized, niche studios (e.g., Pilates, Cycling, Yoga) with a great social experience.

Summary

We recommend avoiding mid-tier operators and studios. The mid-tier category has shrunk over the past decade and will likely continue to struggle given increased competition from low-price and high-end operators. Studios have ‘fad’ like tendencies as concepts come and go and the 4-wall economics are challenging. We prefer to invest in best-in-class high-end operators that have differentiated their offering such as Life Time and low-price players who have disrupted the category and have a proven track record. Despite positive industry trends and expected continued membership growth, there will be winners and losers, highlighting the importance of choosing the right players in the right categories.